There is a lot of work involved in writing these articles. Most of my work is free but if you like what I do please consider supporting me.

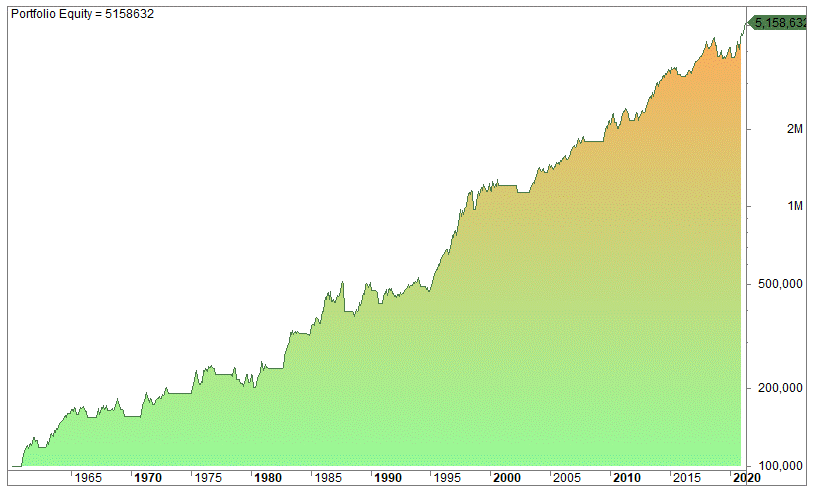

Back in 2012 Meb Faber published a paper called A Quantitative Approach To Tactical Asset Allocation in the Journal of Wealth Management. Meb Faber found the 200-day moving average useful and decided to look at the following simple trend following system in the S&P 500 based on the 200-day moving average:

Go long the S&P 500 when the price crosses the 200-day moving average, and sell when it crosses below the 200-day average. This is probably not the most sensational strategy, to say the least. However, Faber’s article is a great read because of his “simple” ideas, yet very powerful.

Please click here to continue reading about the trend following strategy in the S&P 500.