Meb Faber's Momentum/Trend-Following Strategy in Gold, Stocks, And Bonds

Meb Faber, a famous money manager and writer, has several times stated he is a trend follower at heart. Back in 2015, he published an article about momentum and trend-following called Meb Faber's Three-Way Model in gold, stocks, and bonds- a model that Meb Faber found in some research from Ned Davis Research. How has this strategy performed and is it still working?

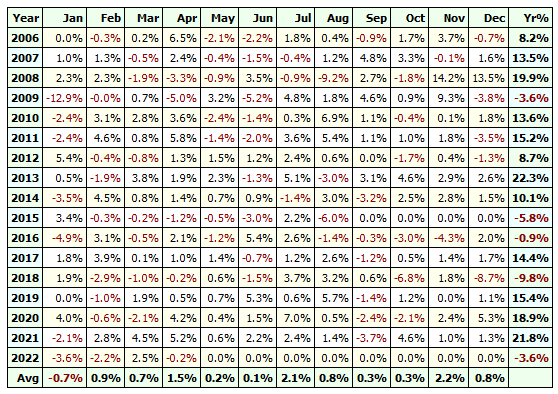

Yes, Meb Faber's momentum/trend-following strategy in gold, stocks, and bonds is still working. The strategy is as simple as it gets: Initiate (or keep) a position if the monthly 3-bar moving average is above the 10-bar moving average. The strategy returned 13% from 1971 to 2015. We updated and backtested the strategy and show you the results after 2015.

Please read here:

Meb Faber's Momentum/Trend-Following Strategy in Gold, Stocks, And Bonds

This is our free newsletter. For a list of the Bonus Articles we have for our Supporting Members, please press here.

Alternatively, you can test our subscription:

Before we go on to explain Meb Faber's momentum/trend-following strategy we start by explaining what momentum investing is:

Thank you for the article! By chance I was also playing around with a Meb Faber type of monthly ETF rotation system. But I chose a more differentiated portfolio of 11 ETFs:

• Equities: VTI, EFA, EEM

• Bonds: BND, BNDX

• Real Assets: DBA, DBB, DBE, DBP, VNQ, VNQI

I buy only the top-ranked ETF based on factoring the 10 months performance and volatility. I also aim for a volatility target and have a stop loss filter. I rotate the ETF on a monthly basis.

Here are the backtest results for the period of 2014-2022:

• CAGR: 19.2%

• Sharpe Ratio: 1.07%

• SPY Correlation: +0.24

• Drawdown: -18.0%

I like this simple strategy, its KPIs and especially the low correlation to the stock market.

What does the expert think?

Thank you. As usual: Great article! I have tested a lot monthly rotation systems and I often see, that the stats worsen, if you test it on daily bars. Same here: the max DD increases from 18 % to 24 %, the Ulcer Index increases from 0,8 to 4,3. At least for me, I find the daily stats more relevant, because I will definitely look more often into my positions than just once a month.