Profitable Williams %R Strategy For Mean Reversion Trading (Only 2 Rules)

Today, we show you a profitable Williams %R strategy for mean reversion trading. It has worked for stock indices such as the S&P 500 and the Nasdaq 100.

There is a common misconception that performance is a direct result of complexity. We are often told that to beat the market, we need high-frequency algorithms or dozens of overlapping indicators.

However, the data suggests that the opposite is often true. Some of the most robust systems are incredibly simple, relying on just one or two rules to exploit core market behaviors like mean reversion.

Today, we’re looking at a Williams Percentage R strategy that boasts a 72% win rate on the Nasdaq 100 (QQQ) while being invested in the market only 21% of the time.

The Core Philosophy: Mean Reversion

This strategy is built on the principle of mean reversion. This concept suggests that when prices deviate significantly from their average (becoming “oversold”), they have a high probability of “snapping back” toward the mean.

This behavior has been a reliable characteristic of the stock market since S&P futures trading began in 1982.

The Mechanics: Williams Percentage R

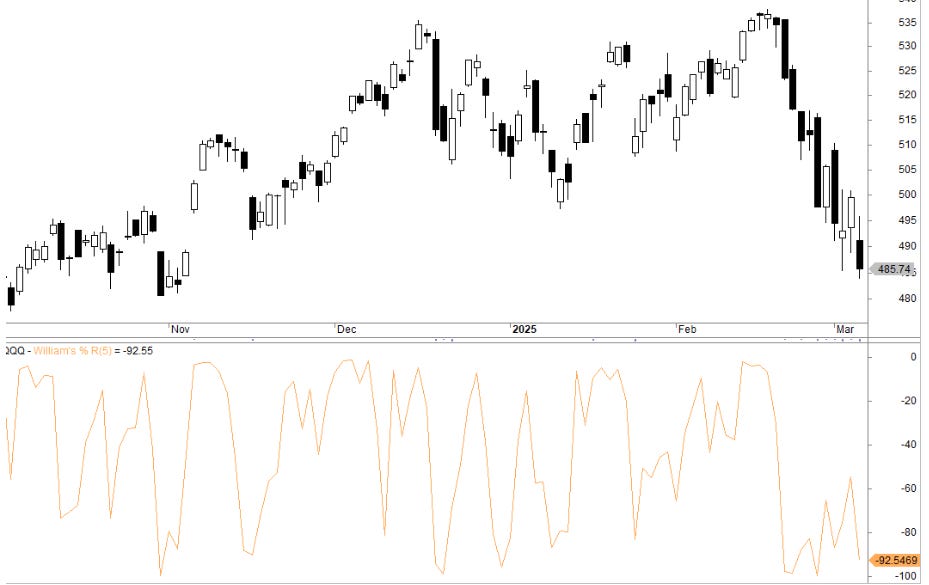

To identify these oversold moments, we use the Williams Percentage R (%R), a momentum indicator that oscillates between 0 and -100. It measures the relationship between a stock’s closing price and its high-low range over a specific look-back period.

For this strategy, we use a 5-day look-back period. Below you see

The Williams %R Two-Rule System

The beauty of this strategy lies in its simplicity. It consists of only two systematic rules:

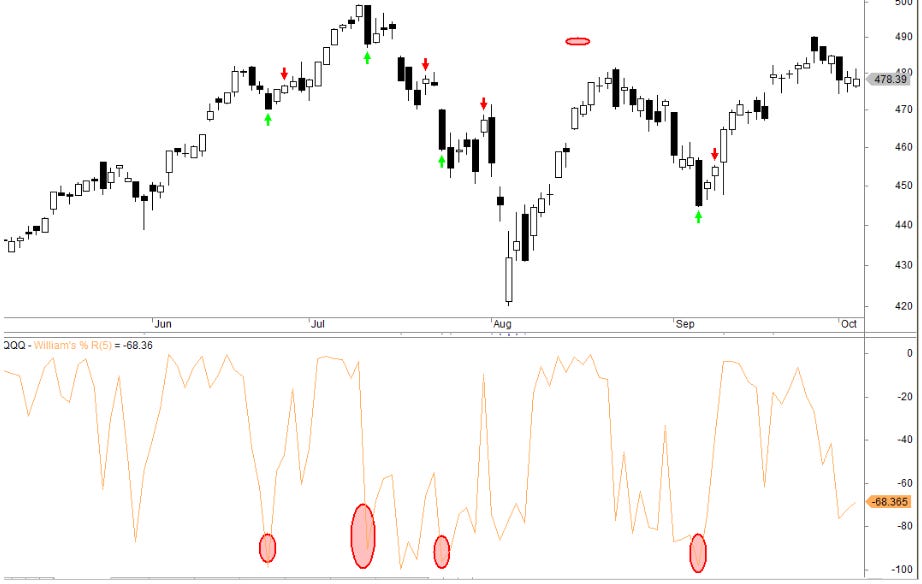

The Entry (Buy): Buy when the 5-day Williams %R closes below -90.

The Exit (Sell): Sell when the closing price is higher than the previous day’s high.

It is truly that simple: no complex filters or secondary confirmations required.

Below you can see a few trades (green arrows for buy and red arrows for sell):

The Data: Why “Low Exposure” is a Secret Weapon

When backtested on the QQQ from its inception to the present, the strategy produced an 11.5% annual return.

At first glance, a beginner might dismiss an 11.5% return as too low. However, looking at the absolute return in a vacuum is a mistake. You must consider the market exposure.

Because this strategy is only in the market 21% of the time, it achieves that 11.5% return while remaining in cash for roughly 80% of the year. If you adjust the return for this limited exposure, the effective return while in the market is approximately 55%.

The advantages of low exposure include:

Reduced Risk: You aren’t exposed to “black swan” events or overnight market crashes for 80% of the year.

Capital Efficiency: Because the strategy is rarely active (averaging only 15 trades per year), you can use your capital for other non-correlated strategies, effectively “stacking” your returns.

Psychological Ease: With an average gain of 0.9% per trade and a high win rate, the “emotional tax” of trading this system is very low.

Risk Management: The “No Stop Loss” Controversy

One of the most interesting aspects of this strategy is that it does not use a stop loss.

In mean-reversion trading, traditional stop losses can be problematic because they often trigger just as the price is about to snap back, locking in a loss at the worst possible time.

In over 20 years of QQQ data, the strategy’s biggest single-trade loss was 18%, and only one trade exceeded a 10% loss.

Rather than using a hard stop, the sources recommend managing risk by trading smaller position sizes and diversifying across different asset classes.

Where Does the Williams %R For Mean Reversion Trading Work?

This strategy is specifically designed for assets that revert to the mean. It works exceptionally well for stock-based ETFs like the QQQ and S&P 500.

However, it is important to note that it does not work well on commodities or metals, as those assets behave differently than stocks. You cannot expect one simple strategy to work on every asset class, and that is okay.

Final Thoughts

The goal of trading isn’t to be in the market 24/7; it’s to be in the market when the odds are heavily in your favor.

By waiting for deep oversold signals (Williams %R < -90) and exiting at the first sign of strength, you can capture significant gains with minimal time at risk. The Williams %R strategy for mean-reversion trading has worked well so far.

👍

The strategy presented on YouTube: https://www.youtube.com/watch?v=v94sNv-Ffi8