Value vs. Growth Rotation Strategy

Today, we look at a value vs. growth rotation strategy.

Few debates in investing are as persistent as value vs. growth.

Value investors look for stocks that appear undervalued relative to fundamentals.

Growth investors look for companies with strong future growth potential, often accepting higher valuations in exchange for faster expected earnings expansion.

But the more interesting question is not necessarily “Which is better?”.

A better question may be:

Can Investors Rotate Between Value and Growth?

A value vs. growth rotation strategy tries to avoid being permanently locked into one investing style. Instead of always owning value stocks or always owning growth stocks, the investor uses a rule-based system to switch between the two.

The goal is simple:

Own growth when growth is leading. Own value when value is leading.

This type of strategy is attractive because value and growth often perform differently depending on the market environment.

Growth stocks may dominate during strong bull markets, especially when interest rates are low and investors are willing to pay up for future earnings. Value stocks may perform better when investors prefer cheaper, more established, cash-generating companies.

What Are Value Stocks?

Value stocks are companies that trade at relatively low prices compared with fundamentals such as earnings, book value, dividends, or cash flow.

Typical value characteristics include:

Lower price-to-earnings ratios

Lower price-to-book ratios

Higher dividend yields

More established business models

Less market excitement

The Quantified Strategies article describes value investing as buying undervalued stocks with strong fundamentals, expecting the market to eventually recognize their value.

In plain English, value investors are usually asking:

“Is this stock too cheap compared with what the business is worth?”

What Are Growth Stocks?

Growth stocks are companies expected to grow revenues, earnings, or market share faster than the average company.

Typical growth characteristics include:

Higher revenue growth

Higher earnings growth expectations

Higher valuations

Lower or no dividends

More exposure to technology, innovation, or expanding markets

Growth investing focuses less on whether a stock is cheap today and more on whether the company can become much larger in the future. The linked article notes that growth investors often buy companies with strong future growth potential, even if valuation is already high.

Growth investors are usually asking:

“Can this company compound fast enough to justify today’s price?”

Value vs. Growth: Which Performs Better?

The answer depends heavily on the time period. However, longer-term historical evidence has often favored value. Data suggests that since 1926, value investing has dramatically outperformed growth investing over the very long run.

That creates the central problem:

Growth Can Win for Years - Value Can Win Over Decades

This is exactly why a rotation strategy is interesting.

A permanent value investor may suffer through long stretches when growth dominates. A permanent growth investor may suffer when markets rotate toward cheaper, more defensive companies.

A rotation strategy attempts to solve this by following relative strength rather than ideology.

The Core Idea Behind a Value vs. Growth Rotation Strategy

A value vs. growth rotation system compares the performance of value stocks against growth stocks and invests in the stronger group.

A simple version might use two ETFs:

Growth ETF: for example, a Russell 1000 Growth or small-cap growth ETF

Value ETF: for example, a Russell 1000 Value or small-cap value ETF

The rotation rule could be based on relative momentum:

Measure the recent performance of the growth ETF.

Measure the recent performance of the value ETF.

Invest in whichever ETF has performed better.

Rebalance monthly, quarterly, or based on a trend signal.

The linked article emphasizes the usefulness of backtesting for comparing value and growth strategies, identifying risk-return profiles, and seeing how each performs under different market conditions.

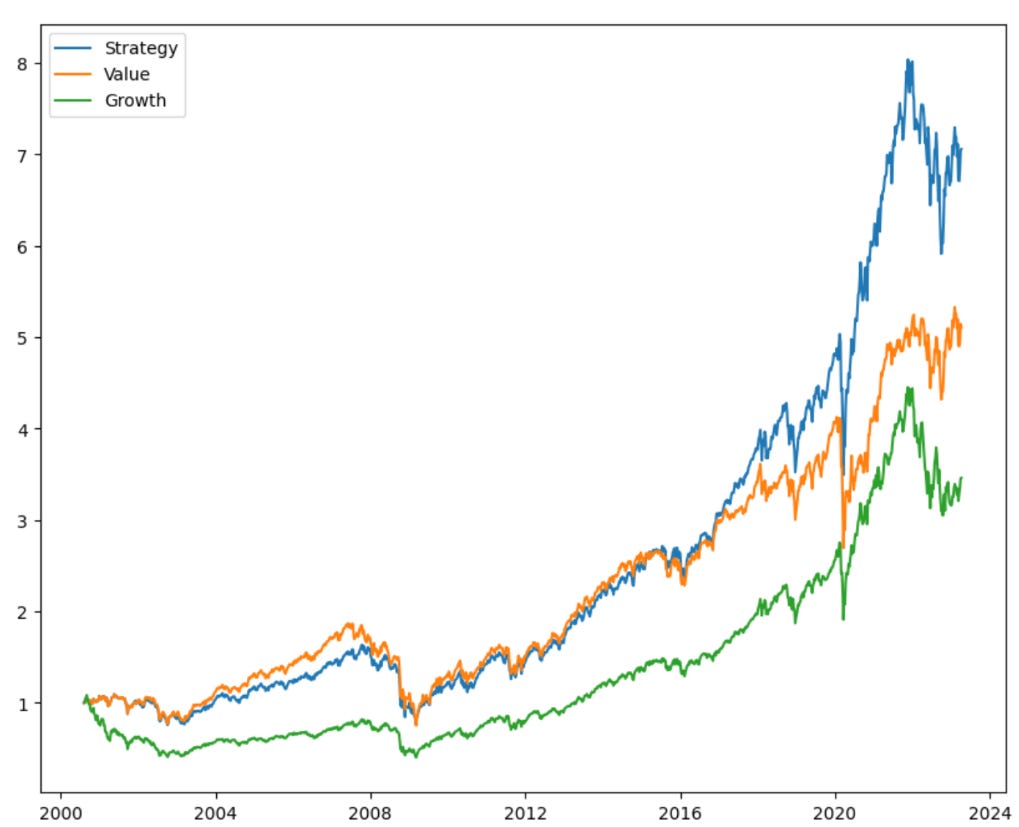

Value vs. Growth Rotation Strategy - Backtest

For the rotation system, we will use the IUSV (value) and IUSG (growth) ETFs (see the trading rules at the bottom of the article).

We started the backtest in 2000, right at the peak of the tech bubble. The data is adjusted for dividends and splits. Here are the returns and performance:

Performance

No. of trades: NA

Average gain per trade: NA

Win ratio: MA

Profit factor: NA

Annual returns (CAGR): 8.96% (value 7.42% - growth 5.60%)

Exposure/time in the market: 100%

Risk-adjusted return: NA

Max drawdown: 52.75% (value 59.71% - growth

62.82%)

Pros of a Value vs. Growth Rotation Strategy

1. It avoids style loyalty

Many investors become emotionally attached to one investing style. A rotation system is more flexible. It does not care whether value or growth “should” win. It follows the data.

2. It can adapt to market cycles

Value and growth leadership changes over time. A rotation model attempts to participate in the stronger trend.

3. It may reduce long periods of underperformance

The article notes that value has experienced a long drawdown relative to growth since around 2007 in many markets and sectors. A rotation strategy may help reduce the pain of staying with the wrong factor for too long.

4. It is easy to implement with ETFs

Investors do not need to pick individual stocks. A rules-based ETF approach can provide broad exposure to each factor.

Cons of a Value vs. Growth Rotation Strategy

1. It can whipsaw

If value and growth keep switching leadership, the strategy may trade too often and underperform.

2. It may create taxes and costs

Frequent rotation can trigger taxable events and trading costs. This matters especially in taxable accounts.

3. Backtests can be misleading

A strategy that worked historically may fail in the future. Overfitting is a real risk.

4. It may miss sharp reversals

Momentum-based rotation systems often react after leadership has already changed. They can be late.

Value vs. Growth and Risk

Growth stocks are often considered riskier because they rely more heavily on future expectations. If expected growth disappoints, valuations can compress quickly.

Value stocks may appear safer, but they have their own risk: the value trap. A cheap stock may be cheap for a reason. The linked article also warns that many lowly valued stocks can turn out to be poor long-term investments rather than bargains.

So the risk trade-off is not simple.

Growth risk is often valuation risk.

Value risk is often business-quality risk.

Final Thoughts: Build a Strategy, Not an Opinion

The value vs. growth debate will never disappear. Some investors will always prefer cheap stocks. Others will always prefer fast-growing companies.

But markets do not reward opinions. They reward process.

Trading Rules

We used the following trading rules: